Valuetronics’

current price of $0.62 represents a potential 26.6% upside, based on a 12-month

target price of $0.785. The target price was derived based on a blended

discounted cash flow (DCF) and relative valuation approach.

Company

Overview

Valuetronics

is an electronics manufacturer headquartered in Hong Kong. It operates in two

segments, the Consumer Electronics segment and the Industrial & Commercial

Electronics segment. The CE segment accounts for c.37% of revenue, and c.63% of

revenue is derived from the ICE segment. The company’s products include smart

lighting, printers, automotive products and medical equipment.

FY2020

Q1 Earnings Review

Trade

tensions continue to adversely impact Valuetronics, as revenue declined by 7.1%

from 704.0 mil HKD to 654.3 mil HKD, while gross profit margin expanded

slightly from 15.6% to 15.1%. Net profit fell from 49.7 mil to 48.1 mil HKD,

while net profit margin increased from 7.1% to 7.4%.

Investment

Thesis

Trade

war fears overblown, new factory in Vietnam to mitigate tariff impact – US-China

trade tensions has an adverse impact on Valuetronics, given that c.45% of the

company’s revenue is derived from US shipments, and approximately half of the

company’s shipment from China to the US is subjected to the 25% tariff imposed

by the US.

However,

Valuetronics has been working to mitigate the adverse impact of tariffs by

building up its production facilities in Vietnam. Mass production has started

since June 2019, and shipments have been made from Vietnam to the US market.

The company also intends to acquire a plot of land in an industrial park in

Vietnam to build a manufacturing campus, further boosting production capacity,

and diversifying its production base beyond China.

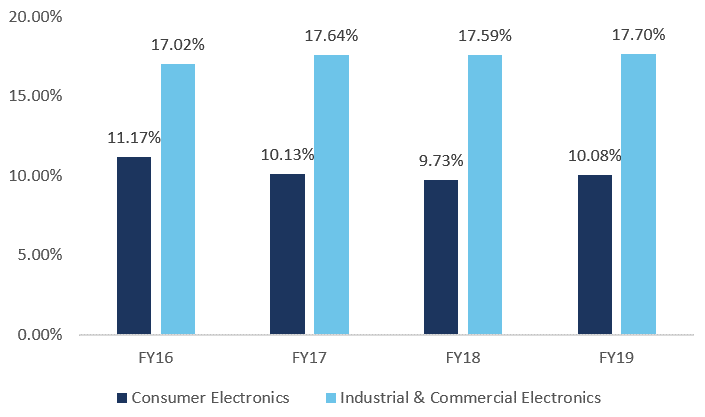

Rebound

in demand for smart lighting – Valuetronics produces smart lighting for

Phillips, under its Consumer Electronics segment. Demand for smart lighting is

set to increase globally, which would potentially drive a rebound in revenue

for Valuetronics’ CE segment, which has seen revenue declining over the past

two years.

As

of 2018, the global smart lighting market stood at US$6.87 billion, and is

forecasted to grow at a CAGR of 22.67% from 2019 to 2025 (Source:

IndustryArc). The main driver of this demand is the trend towards smart

homes and smart cities, and the increased emphasis on sustainability issues.

The Asia-Pacific region accounted for 37.36% of the global smart lighting

market in 2018, and is likely to continue to see sustained demand, due to

rising disposable incomes among the population. Valuetronics is well positioned

to benefit from this trend, given that its production facilities are based in

China and Vietnam.

Solid

net cash position reduces downside risk, facilitates acquisitions – Net

cash position constitutes c.66% of its market capitalisation. With an ex-cash

P/E ratio of 2.9x, the market is severely under-pricing the company’s future earnings.

The cash pile also supports potential acquisitions, as the management has

guided that it intends to deploy the cash pile for growth opportunities, in

line with the group’s strategy to explore M&A opportunities in North

America.

Catalysts

Positive developments from the US-China trade

negotiations –

Valuetronics has been on a downtrend since its peak of $1.08 in early 2018,

mainly due to fears of tariffs impacting its products exported from China.

Progress in US-China trade talks would provide tailwind for Valuetronics.

Key

Risks

Escalation

of US-China Trade War – Currently, c.50% of Valuetronics’ revenue is

derived from shipments to the US, and around half of this is subjected to the

25% tariffs imposed on electronics manufactured in China.

Foreign

Exchange Risk – Valuetronics reports its financials in HKD, while being

traded in SGD on the SGX. Currently, the HKD is pegged to the USD and allowed

to fluctuate within the 7.75 to 7.85 range. With the recent political

uncertainty, there is some risk that the HKMA may be unable to defend the peg.

In the unlikely scenario that the HKMA adjusts the band upwards, there would be

currency risk if the HKD weakens against the SGD.

Valuation

The

Discounted Cash Flow valuation for Valuetronics was $0.83, using a conservative

terminal growth rate of 1.0% on a terminal year free cash flow of c.100 mil HKD, after accounting for c.80 mil HKD of annual capex.

Weighted Average Cost of Capital (WACC) was derived to be 8.81% using the

Capital Asset Pricing Model. Valuetronics does not have any borrowings, hence

its WACC is entirely dependent on its Cost of Equity.

Based on relative valuation, Valuetronics trades

at a discount to its peers. While Venture Corp is significantly larger than

Valuetronics based on its market capitalisation, at current valuations, the

market has imposed an unfairly high small-cap risk premium on Valuetronics. Based

on a consensus forward earnings of $0.073 for Valuetronics, a forward P/E of

10.1x based on its peer group mean implies a valuation of $0.74. Relative

valuation metrics for comparable companies in the electronics manufacturing

sector are shown in the table below.

Conclusion

Using a simple average of the two valuation

methods, a target price of $0.785 is obtained. This represents a 26.6% upside

from the current price of $0.62.

If you enjoy reading my articles, please 'like' my Facebook page to receive all the latest updates. It would also mean a lot to me if you could share my articles on Facebook. Thanks! :)