Markets rallied strongly over this short trading week, with

US indices entering a bull market, which is defined as a >20% gain from the

bottom. Optimism over the potential flattening of the curve in US and Europe,

along with further stimulus from the Fed helped markets recover from their lows

2 weeks ago. Overall, my portfolio is down about 10% based on cost. Here’s my

updated portfolio as of 9 April 2020:

DBS – The bank has been aggressively buying back shares

since January, spending in excess of $400 million, which is greater than the full

year amount spent in the past 4 years. DBS’ AGM has been postponed, which means

the final dividend would be delayed. There is a concern that as Stanchart and

HSBC have scrapped dividends due to the uncertainty ahead, DBS would follow

suit as well. While Stanchart and HSBC were told by UK Regulators to scrap their

dividends, DBS has not faced a similar advisory from MAS. MAS has indicated

that “sustaining lending activities should take priority” and that the “release

of capital buffers should not be used to finance share buybacks during this

period”. However, given the amount of money that had been spent on aggressive

share buybacks, and a cut in dividends would not bode well with investors. This

was a question I wanted to raise at the AGM, but that would not be possible for

now.

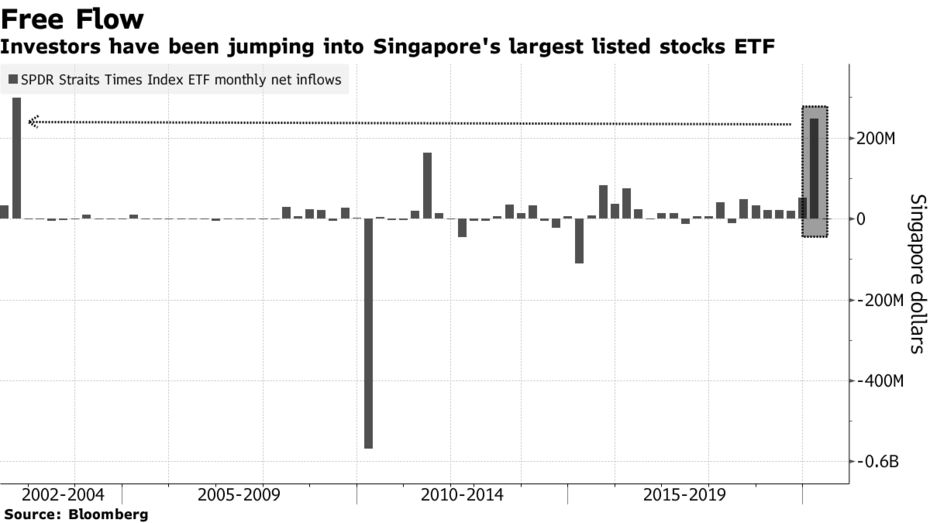

SGX – With the recent market volatility, trading volumes

have shot through the roof which benefits SGX. Securities daily average value

(SDAV) for March more than doubled year on year to $2.19 billion, while ETF

turnover increased eight fold to $1.2 billion for March. Interestingly, investors

have been pouring money into ETFs, with the inflows for the STI ETF as the

highest level since 2002 (refer to chart below). Structured warrants and DLC

value traded also rose by 76% year on year. With more volatility expected ahead,

SGX stands well positioned to benefit from the increased trading activity –

which is great – whether investors gain or lose, SGX still makes money!

|

| Source: Bloomberg |

SATS – Further support measures for the aviation sector provided

some relief for SATS’ share price, which had been battered down by the Covid-19

crisis. Aviation remains a strategically important sector for Singapore, hence

there are vested interests to ensure that SATS is able to weather this

unprecedented challenge. Recently, SATS also managed to borrow $200 million due

2025 at 2.88%, a relatively favourable rate which indicates the market’s

confidence in SATS’ financial strength. Interestingly, SATS bought back shares

at around the $2.81 to $3.04 range immediately after raising debt on 31 March,

which may indicate the management’s view that the company’s shares are undervalued.

Between 1 to 7 April, SATS purchased a cumulative total of 535,000 shares.

I have written more about SATS here:

Mapletree Commercial Trust – This is a REIT that I’ve been

following for a long time, hence I entered at $1.61 which I feel is a

reasonable price. MCT’s revenue exposure to VivoCity is around 45%, which would

be severely impacted by the circuit breaker measures. However, the rest of MCT’s

assets are office properties, which would be less affected, apart from commercial

tenants that have to wind up due to the downturn. In the long term, I believe that

the development of the Greater Southern Waterfront precinct would benefit MCT,

hence I would be ready to increase my position if the opportunity arises.

If you're keen to learn more about REITs, I have written two posts here:

ETFs – Averaged down on STI ETF at $2.49 and entered a new

position for 2800.HK at 24.05 HKD, which tracks the Hang Seng Index. To me, ETFs

are positions that I intend to hold forever, so volatility does not matter to

me. In fact, because I don’t intend to cash out on my positions, I treat them as

more like ‘bonds’ and simply collect a 4 to 5% yield into perpetuity, which is

decent enough for me. I have wrote some brief thoughts on the valuations of the

various HSI sub-segments here:

My foray into ETFs is primarily driven by two reasons. First,

we only can evaluate if we have outperformed the market based on hindsight. Let’s

say 20 years from now, we realise that we are not as great of an investor as we

perceived, and have underperformed the market. By then, it would be too late to

realise that you would have been better off with a passive investment portfolio.

Therefore, having a proportion of my portfolio in diversified ETFs serves as an

‘insurance’, to ensure a part of my portfolio gets the market return in the

long run. The second reason is more practical – if I were to work in the

finance sector in the future, it is likely that trading restrictions would be

placed on individual stocks, whereas ETFs would still be allowed. Hence, it

would be good for me to get some ETF exposure early.

I am looking to diversify my ETF holdings to track 3 main indices

– STI, HSI and the S&P500.

Watchlist

I’m looking at US financials/tech, and maybe 1 or 2

Singapore REITs to add to my portfolio. Would probably be funded by cash and

proceeds from a potential divestment of Singtel, Jumbo or Hanwell.

Thoughts on the current market

Honestly, your guess is as good as mine with regard to the Covid-19

situation. While the current slump started off as a healthcare crisis, it quickly

resulted in a financial crisis as businesses remain shut and trade slowed. Globally,

we would probably see the lockdown measures extend for at least another month

or two. And experts have warned about the risk of infections rising again if

the social distancing measures are relaxed. Personally, I believe that the US

mortgage market is at risk, given that it was reported that one third of

tenants failed to pay their rent in March. As unemployment soars in the US,

more people are unable to pay their rent, which in turn results in mortgage

backed securities at risk. While the Fed has shown their ability to intervene

in the mortgage market, there is only so much they can do.

Nonetheless, for equities, I am constantly on the lookout

for bargains. While for ETFs, I am more comfortably with a dollar cost average

strategy as I take a long term view. I would continue to consolidate my

portfolio by trimming underperforming positions and averaging down on high conviction

bets, while initiating new positions in companies that I find attractive. Overall,

I want my portfolio to emerge from this crisis stronger.

Disclaimer: This article is intended for informational and discussion purposes only, and do not constitute financial advice. When in doubt, please contact a licensed financial adviser.

If you enjoy my articles, please 'Like' my Facebook Page at: https://www.facebook.com/AlpacaInvestments/

Disclaimer: This article is intended for informational and discussion purposes only, and do not constitute financial advice. When in doubt, please contact a licensed financial adviser.

If you enjoy my articles, please 'Like' my Facebook Page at: https://www.facebook.com/AlpacaInvestments/

Follow me on Instagram at @AlpacaInvestments

Hi. Appreciate your detailed sharing very much. In view of the current virus situation, what your views on FPL? I am quite interested in its dividends and low valuation but it seems to have a sizable exposure to retail property and development properties in Australia, which are quite gloomy now. Is there any updates from the management regarding the distribution this year? Thanks.

ReplyDeleteHi AlpacInvestments, can you share with US stocks are in your watch list? I saw that Australia banks have fallen a bit, are that in your radar as wellhttps://alpacainvestments.blogspot.com/logout?d=https://www.blogger.com/logout-redirect.g?blogID%3D693329366744164363%26postID%3D3136823996460087726?

ReplyDelete