In this article, I’ll be taking a detailed look at the revenue drivers for SATS Ltd – on the factors that drive the company’s revenue. I was inspired to write a post on breaking down the revenue drivers for SATS, after reading a post on Wall Street Oasis. I was on the forum to find out more about working at an asset management firm, and came across a post that shared about how fund managers evaluate investments – with a strong emphasis on the P&L of the company. Basically, when projecting revenue and profits, the analysts would attempt to breakdown the revenue into segments and arrive at a certain price x quantity for each segment. I would attempt to apply the same framework to analysing SATS.

Business Overview

SATS is a leading provider of gateway services and food solutions in Asia. As the main ground handling service provider at Changi Airport, it derives its revenue from two main segments – gateway services and food solutions. Its geographical reach covers 13 countries in the APAC region, although Singapore accounts for 82.4% of total revenue, hence the success of SATS is closely tied with that of Changi Airport. The aviation sector accounts for 85% of its revenue, from providing in-flight catering, baggage handling and other services to airlines.

There is a misconception that SATS is a monopoly. In fact, the contracts for ground handling services for airlines at Changi Airport are subject to open tenders, and there was a price war back in 2016 which eroded profits. However, SATS controls nearly 80% of the ground handling market at Changi Airport, with Dubai’s dnata controlling the other 20%. This 2016 report provides a good overview of the competitive landscape and market dynamics between the two service providers.

Financials

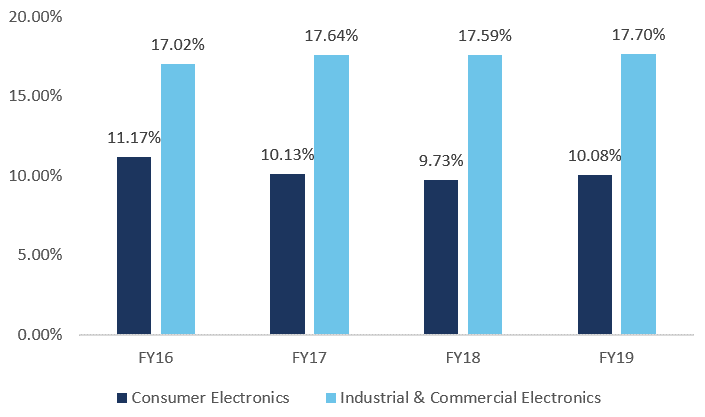

At first glance, it appears that SATS’ revenue has been rather flat for the past 5 years, while profit has been increasing year on year, which is mainly due to increasing net profit margins. The management has increased dividends every year as well. However, by looking at the contributions from both segments, it is evident that revenue from the Aviation segment has been growing, while revenue from the Non-Aviation segment has been declining. Hence, there is strong evidence to support the thesis for SATS to be driven by growth in air travel in the region.

Key drivers of revenue and profit

SATS’ performance is heavily dependent on the number of passengers travelling though Changi Airport. This includes both inbound and outbound tourists, and transit passengers. Changi Airport has started works to construct a new Terminal 5, scheduled for completion in 2030. This new terminal would significantly increase Changi’s annual passenger capacity, from 82 million currently to potentially 150 million passengers a year. Given that SATS’ strong track record as the leading ground handling and in-flight catering service provider, the increased passenger volume would benefit the company if it is able to maintain its dominant market share.

1. Inbound Tourism to Singapore

|

| Source: CAAS, Singstat |

Singapore’s attractiveness as a tourism destination is a key driver of revenue for SATS. I obtained the inbound tourism statistics for Singapore over the past 10 years, to identify trends in tourism figures from different regions. I have highlighted the subtotals for each region. As seen in the table above, I believe that SATS has been riding on the growth of air travel in the region, with the largest increase in passengers from China and Southeast Asia, which have more than doubled since 2008. The figures from North America are low, because the statistics from CAAS only accounts for country of embarkation, and I believe most tourists originating from North America would transit either in Japan, Korea or Hong Kong, en route to Singapore.

I think the key question here is how much more can the aviation market here in Asia grow – and I believe that SATS would be a good proxy for rising affluence in Southeast Asia which increases demand for air travel. Another factor to note would be the strength of the currencies for these countries, as this would affect decisions to tourists to take overseas holidays. For example, the recent weakness in the Chinese Yuan may dampen demand for overseas vacations.

Recently, the ongoing political situation in Hong Kong has resulted in a short term increase in tourist arrivals due to Chinese tourists preferring Singapore over Hong Kong as a vacation destination, though the longer lasting effects may be more uncertain.

2. Outbound Travel from Singapore

|

| Source: ICA, Singstat |

Singaporeans traveling overseas for holidays are another key revenue driver for SATS. Figures from SingStat shows that outbound travel from Singapore has almost doubled over the past decade, from 4.9 million to 8.4 million trips annually. As the figures from SingStat is titled “outbound departures from Singapore”, my assumption here would be that this figure includes both business and leisure travelers.

The key driver of outbound travel here would be the strength of Singapore’s economy. Obviously, people would take more overseas holidays if the economy is doing well, together with more business trips. Recently, the economy appears to be slowing down, as seen from the reduction in bonus for civil servants as well as hearing from friends who are facing a tough job market as fresh grads. Furthermore, given Singapore’s position as a developed economy, I believe that there is less room to grow for outbound air travel as compared to inbound and transit passengers.

3. Transit passengers

Figures from SingStat define “transit passengers” as those who arrive and depart on the same plane within 24 hours, which probably refers to planes that stopover for refueling and allowing some passengers to disembark, while picking up new passengers. Hence, the reported figure for “transit passengers” are extremely low, at around 700,000 annually. Personally, I would define “transit passengers” as those who do not cross into our customs border, for example, flying from Europe with a layover at Changi Airport and departing for Australia. This definition of transit passengers would account for a much larger proportion of passengers through Changi Airport than the reported figure, and should probably account for the difference between the total number of passengers handled by Changi after subtracting inbound and outbound tourists. As discussed later, a risk regarding transit passengers would be the introduction of ultra long haul flights which bypass Singapore.

4. Investments in Technology

Here I’ll be looking at the trends in operating costs for SATS as a percentage of revenue. From the table above, it is evident that staff costs having been taking up a larger proportion of expenses, while cost savings have been driven by reduced raw material costs. SATS has been investing in technology to boost efficiency, and ideally this would have translated into costs savings which would support its rising profit margins over the past 5 years from 10% in FY2015 to 14% in FY19. For example, SATS introduced augmented reality glasses to its ground handling staff for ramp operations, boosting productivity by improving the efficiency and accuracy of the baggage and cargo loading process.

Given the expansion plans for Changi, SATS’ staff costs would increase significantly as it hires more ground handling staff, and ongoing investments in technology can help to mitigate the impact of rising staff costs by increasing productivity. Going forward, an indicator to watch would be SATS’ staff costs as a percentage of revenue, to determine if the investments in technology have paid off.

Risks

Uncertain economic outlook due to trade tensions may dampen tourism numbers – Mainland Chinese visitors have been a major contributor to Singapore inbound tourism numbers. The ongoing US-China trade war may negatively affect economic sentiment, reducing tourist arrivals to Singapore.

A recurring point that I’ve observed in prior earnings releases would be that “higher oil prices results in pricing pressures for SATS”. I am unsure of the direct effect of oil prices on the price which SATS charges airlines for its in-flight catering and ground handling services. The only possible causal link that I can draw would be that airlines would attempt to reduce spending on SATS’ services when oil prices are rising, in a bid to reduce costs. Perhaps existing shareholders may want to clarify with the management on how rising oil prices leads to pricing pressure for SATS, and please write to me if you have the answer!

I think a huge risk, though unlikely, that is seldom mentioned is Singapore losing its competitiveness as a regional aviation hub. While the likelihood of this occurring is low, the risk of Singapore losing its competitiveness as an aviation hub would be extremely detrimental to SATS. Currently, Singapore serves as a stopover point for flights between Oceania and Europe and Southeast Asia. Currently, the technology that makes ultra long haul (~ 20 hours) flights possible exists, which was recently on trial by Qantas.

However, as discussed in this YouTube video (https://www.youtube.com/watch?v=TNUomfuWuA8), the financial aspects of ultra long haul flights may not be that lucrative for airlines at the moment. There’s also the issue of passenger preferences. After all, who would want to sit in an economy class seat for 20 hours straight? Nonetheless, in the future, there is the possibility that improvements in aircraft technology and changes in passenger preferences may increase demand for ultra long haul flights, and erode Singapore’s relevance as a regional hub by bypassing Changi Airport. Personally, I would rate this risk as low, similar to how there have been plans for the Kra Canal across southern Thailand, which would allow ships to bypass the Malacca Strait and threatening Singapore’s position as a shipping hub. However, this has yet to materialise after it has been discussed for decades.

Going Forward

During SATS’ capital markets day presentation earlier this year, their management had indicated that it has plans to ramp up capital expenditures over the next 3 years, with projected investments of $1 billion, to be mainly funded by debt. The management also targets an increase in gearing to a 30% debt to equity ratio within the next 3 to 5 years. I believe that this is a positive step for the company, given that its current gearing level is extremely low at a net debt to equity position of 0.07. Taking on debt to fund investments would allow the company to take advantage of low interest rates to drive growth.

Conclusion

I hope this article provides a good starting point for current and potential investors in SATS to evaluate its business. Overall, I believe that SATS is an extremely well managed business with positive macro factors driving the business. Although the current valuation isn’t ‘cheap’ to me, Warren Buffett once said that “It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price”, and I believe SATS would be considered as the former.

Lastly, I feel that this would be a good time to update my portfolio. Do check out the ‘My Portfolio” tab to see my latest holdings!

Note: I do not hold shares in SATS at time of writing.

If you enjoy reading my articles, please 'like' my Facebook page to receive all the latest updates. It would also mean a lot to me if you could share my articles on Facebook. Thanks!

Note: I do not hold shares in SATS at time of writing.

If you enjoy reading my articles, please 'like' my Facebook page to receive all the latest updates. It would also mean a lot to me if you could share my articles on Facebook. Thanks!