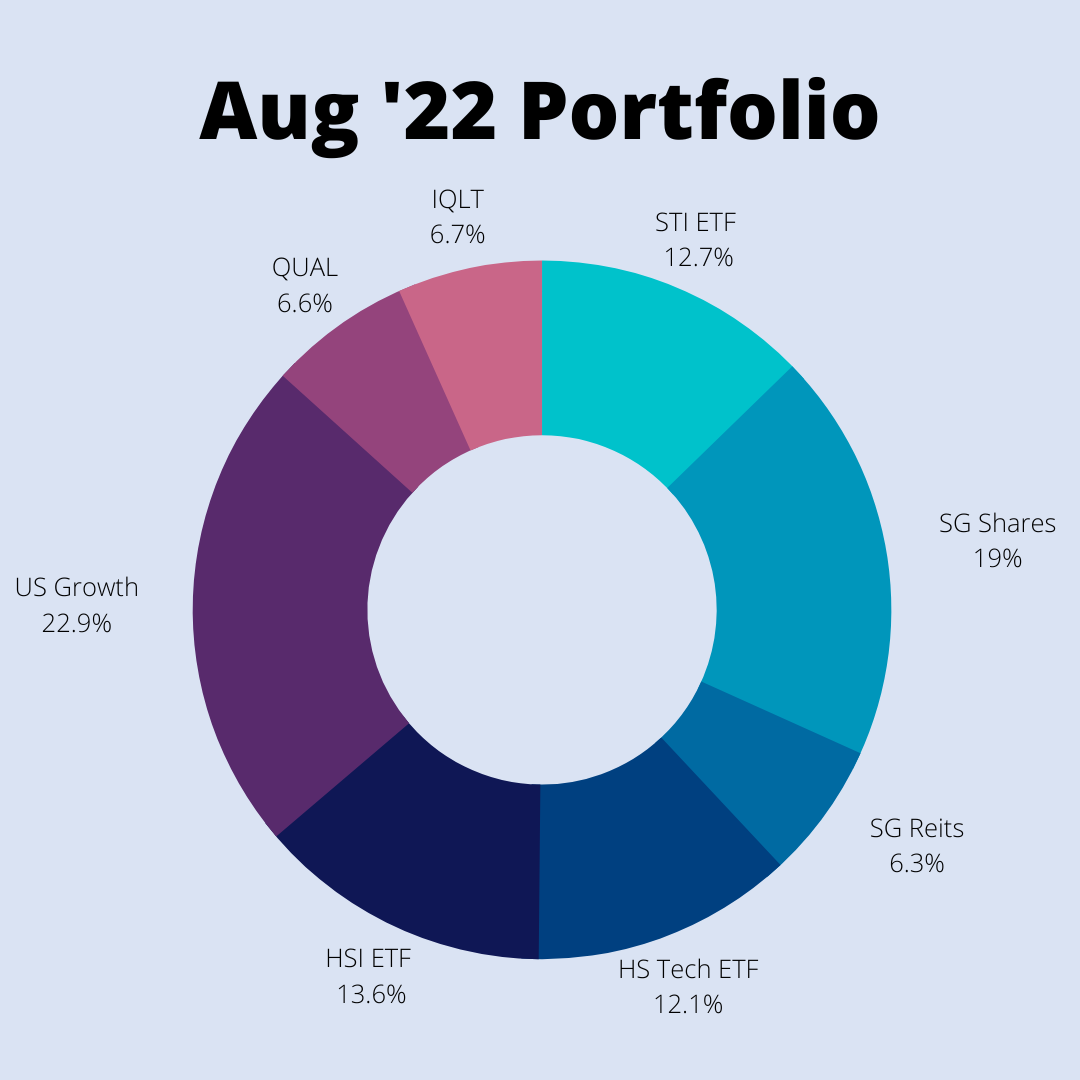

Portfolio allocation as of Nov '22.

• SG Shares: CDG, DBS, SGX, Valuetronics

• SG Reits: Syfe Reit+

• US Growth: BABA, INMD, PYPL, SHOP, TDOC, UPST

Not much to update this month. Apart from adding a few hundred dollars to my Syfe Reit+ position, I did not make any additions to the portfolio. I did try to increase my position in Valuetronics at below $0.50, but was unsuccessful. Perhaps better luck in December.

I think it is ironic that there’s strong interest in the markets only when the market is doing well. Take crypto as an example. I’m not a crypto advocate, but a year ago, literally everyone was talking about crypto; showing off their gains and encouraging others to invest. But today it is very much radio silence from these folks. I’ll be upfront to say that I too got convinced, and lost a manageable amount in Luna and FTX.

Humans are wired to follow the crowd and it often feels uneasy to go against it. One way I try to overcome this would be to remind myself to invest consistently and that given my time horizon, markets should go up in the long run. I have a friend that likes to announce in our group chat whenever there’s a “new YTD low for S&P500”, or that it is a “bad time to invest in the market”. I make an effort to invest a small amount whenever I hear stuff like these. So far, it has worked out well for me.

2022 Dividends collected

I still recall one of my early conversations on dividends – I was 19 at that time, as an NSF, speaking to a guy in his 30s who was doing his reservist. I shared that I invested ~$2k in SingTel, which yielded ~5%, or $100 annually. This person could not understand why I would risk $2k of capital to earn a measly $100. My response was that investing would beat leaving the cash in the bank, with near zero interest rates on savings accounts. He was unconvinced, but this also marked my foray into dividend investing.

Fast forward to today, I've joined the workforce, with an average savings rate of ~80%. I have consistently invested nearly all my excess cash, with a preference for diversified ETFs and dividend-paying stocks. In 2022, I have received ~$2.9k in dividends, and the current run rate for 2023 stands at ~$3.6k (that is, assuming I don't invest a single dollar more). By end 2023, my target would be to generate ~$6k of dividends, which works out to $500/month.

For some context, the $300/month which I receive currently, works out to:

(i) 75 plates of $4 chicken rice, or

(ii) 10 instances of $30 restaurant meals, or

(iii) 20 journeys of $15 taxi rides.

For the record, these are only for illustrative purposes, and I don't do any of these at those frequencies… but every dollar of dividends goes a long way.

I think of FIRE not in terms of a "FIRE number", but rather, a "FIRE cashflow". Cashflow is king, and as long as my passive income can cover my expenses, work becomes optional. Broadly, these are the milestones for the journey. Numbers are in 2022 purchasing power and will be inflation-adjusted along the way:

1k/month, Lean FIRE: Covers my monthly expenses with some buffer. Employed full-time.

2k to 3k/month, Barista FIRE: Potentially able to scale back from full-time employment, and supplement passive income via part-time work or side hustles.

4k/month, Full FIRE: Theoretically, I don't need to work at this point. But I would still want to work, purely out of interest or passion. (Too many ideas to list)

The magic of compounding dividends is probably the 8th wonder of the world. Read more about Why Dividends Matter to me in my previous post.

Random musings on FIRE and life

The art of doing nothing

Earlier this year, I had to take a week of leave due to company policy. I didn’t have plans for that week. It was simply meant to be a break. A common question that I received was “you’re not travelling?”. I found it weird having to justify that I’m simply taking leave to have a break from work. Don’t get me wrong – I enjoy travelling, but I don’t see it as a necessity.

Thus, when I get this question, I usually tell acquaintances that I’m taking leave to “do nothing”. In reality, I think “simplicity” would be a positive way to describe how I spent the week, while “mundane” may be another adjective that carries a negative connotation.

A typical day of my week on leave would start with waking up around 10 am, and then throughout the day, doing a light workout, going for a walk in the park in the late afternoon (before the after-work crowd arrives), practicing a language on Duolingo, and reading a book or some personal finance content. Evenings were mostly for catching up with friends over dinner. All in all, a pretty good mix of me-time and social activities, in my view. Simple or mundane, this is fulfilling enough for me.

One of the “finsta” accounts I follow, @centsofindependence, recently shared about a day in her Barista FIRE life – which involved waking up naturally in the morning, having breakfast with her partner at 11am, spending some time on managing her personal finances and chilling at a bistro in the afternoon while posting some updates to her Instagram page. They also host friends for dinner once or twice at their place during the week. This is a great example of the post-FIRE life that I envision.

I guess to some people, these may constitute “doing nothing” … but who’s to judge what’s right or wrong?

An easy life or a hard life?

I don’t see any issues with wanting an easy life. In fact, I would posit that most people innately want an easy life. But from society’s standpoint, people have been conditioned to think that yearning for an easy life isn’t politically correct, thus most people wouldn’t openly claim that they want to have it easy.

Now, let me add in the caveat that this does not mean shying away from all challenges. To me, looking for an easy life means focusing on things such as the effort-to-reward ratio, looking for “easy wins”, and basically, living the way that makes me comfortable, instead of blindly following society’s definition of what’s “ambitious” or not (which very often, involves judging a person’s “success” in monetary terms).

I’m a competitive person, or I should say, selectively competitive. That means playing to my strengths. Focusing my efforts on things that I’m good at, and are likely to payoff well. If I know that I will breeze through Business School, rather than say, Quantum Physics, then I’d pursue a Business degree for sure. Easy A’s for me. Also, for example, given that I know doing well in competitive sports such as swimming depends on one’s genetics as much as hard work, and hard work alone won’t make me a great swimmer, then I won’t even bother pursuing competitive swimming in school. But I would still swim as a hobby.

A friend had a good piece of advice: if she could make money the easy way or the hard way, she’d choose the easy way, always. Very smart.

Conversely, “hustle culture” perpetuates a mentality which glorifies working long hours, sacrificing sleep, always wanting more and seeing hardship as a badge of honour. Not the type of life I want.

I think quotes such as “Don’t ask for an easy life, ask for a challenging life, and for the strength to overcome these challenges” are complete nonsense. If we could choose to be born as an heir to a billion-dollar fortune, who wouldn’t? Let’s be real here.

“Hardship” shouldn’t be a competition where we compare who is “having it worse”. This type of race-to-the-bottom perspective benefits nobody. We all have our fair share of challenges. Please don’t romanticise adversity.

At this point, you might scoff and say… c’mon, being able to live in Singapore is already fortunate enough. Of course, I recognise the positives we have here – relative wealth, a stable government, good infrastructure and a decent education system. On one hand, the rising property prices could be seen as a testament to our success, but at the same time widens the gulf between the haves and have nots.

On balance, I think it would be naive to claim that youths today “have it easy”. Sure, every generation has its fair share of challenges. But at present, with young couples increasingly feeling like they’re being priced out of the housing market, COE prices near the 100k mark, rising inflation, job market uncertainties and geopolitical tensions, the future looks challenging indeed.

Therefore, one of the main aims I have would be to make my life as “easy” as possible, that is, to live life on easy mode. And this is aligned with my goal of achieving FIRE – to have the safety net, the freedom and options to pursue what I love, and being in control. I believe there will come a point where money, while still important, no longer becomes a priority in life.

And as a secondary “purpose”, to continue writing about financial literacy and help as many people as possible to achieve the same.

To end off my thoughts on this section, a phrase often use would be that “life is already tough enough, think of ways to make life better, not worse”.

A contrasting example

I’ve been writing too much about FIRE, obviously because I’m biased here. Now, let me share a contrasting example where FIRE just does not make sense.

A friend works as a software engineer in a tech startup. They earn roughly twice the salary of an average fresh grad. Their company has a “work from anywhere” policy, which basically means that you could spend a month working by the beach in Bali, a month working from home in Singapore, and then maybe another month working from a hostel in Tallin, Estonia, alongside fellow digital nomads. They enjoy fantastic work life balance, and get additional perks such as food and gym memberships. Crucially, they enjoy what they do and get to work on meaningful and impactful stuff.

When I shared that my goal was to retire early, they mentioned that they don’t think they’ll ever want to retire. Why would this person ever want to stop working? Heck, if I was in that position, FIRE would be the last thing on my mind as well. There is simply no need for FIRE in this situation. By the way, this person is also an astute investor, and will likely hit Financial Independence pretty quickly (even before me). They just don’t have to, or want to Retire Early. A totally valid point of view.

But the key question here would be – how many people do you know that are in this privileged position of being well-compensated, have great flexibility and enjoy the work they do? And taking a step back, are there even enough of these types of jobs to go around, for everyone who aspires to live this life?

I can give you my answer: this is the only person I know with all these perks, and these types of jobs are few and far between. And more often than not, they require specific skills such as coding knowledge, which not everyone is cut out for.

Therefore, I choose to create my own freedom. Onwards and upwards.