In early February, I bought SATS at $4.49. Back then, the

Covid-19 situation seemed to be largely confined within China, with just a few

cases in Singapore. I think at that point of time, most of us would have

expected Covid to blow over fairly quickly, and be able to get on with our

lives.

How wrong were we. And how wrong was I to initiate a

position in SATS in early Feb. Over the next few months, with most countries imposing

travel bans, air travel and tourism were completely decimated. By March, SATS’

share price had collapsed to around $2.50, more than a 50% decline from its

52-week highs.

When I bought SATS at $4.49 in Feb, in theory, it seemed a

pretty straightforward strategy – Covid would surely affect SATS, but if we don’t

know exactly how serious the impact would be, thus it’d make sense to dollar

cost average. My purchase at $4.49 was my first tranche, and I had the ability

to average down one or two more times if necessary. After all, Warren Buffett

said that if one is a net buyer of stocks, then one should be happy that stock

prices are falling, right? But in practice, when the entire market sells off,

when you look at the US market swinging with 5% to 10% moves in a single day,

and you look at your entire portfolio declining across the board, it’s not as

easy to simply stick to your plan.

Now that things have cleared up a little, I’ve spent the

past week looking at SATS again. Make no mistake, fundamentals have changed

drastically. Passenger flights are almost non-existent – in April 2020, at

grand total of 25,200 passengers passed through Changi Airport – a 99% decrease

from a year ago.

Today, it is no longer about projecting revenue growth, or

expecting SATS to even turn a profit in the near term. Instead, it is about

survival – analysing whether SATS would be able to survive the Covid crisis and

emerge stronger.

Here are the reasons why I believe that SATS would be able

to survive the Covid crisis:

1. SATS’ profit guidance released in April estimated that

they would suffer a 50 to 70m loss for Q1 FY20/21.

The estimated 50-70m loss is “after taking into consideration

grants received from governments”.

Given that this is for the 3-month period from April to June

2020, where we are already in full-blown lockdown with a complete ban on all

tourists and transit passengers, I believe that this is as bad as it gets. The

only passengers at Changi Airport are returning Singaporeans, or foreigners

leaving the country. Which make up a grand total of 25,200 passengers.

|

| Source: Changi Airport Traffic Statistics |

2. SATS started off on a strong cash position, and has the

ability to raise more debt

SATS last reported their financial results on 31 Dec 2019.

As at 31 Dec 2019, SATS had 212m in cash and 103.6m in short term and long term

debt, with a debt to equity ratio of 18%.

Note that the increase in debt to equity ratio from a year

earlier was due to recognising changes from IFRS 16. For those with some accounting

background, IFRS 16 is basically a silly rule that requires companies to

recognise their long-term lease liabilities as a liability, instead of

recognising them in their P&L each year. For example, if SATS leases an

office for 10 years, then they would have to record these 10 years worth of

future lease payments as a liability, which distorts the ‘true’ financial

position, because it is not exactly a ‘debt’. Excluding the impact of IFRS 16, SATS

noted that their ‘actual’ debt to equity ratio still remains at 6% as at 31 Dec

2019.

Subsequently, SATS announced that they completed the

acquisition of Monty’s Bakehouse, for a total consideration of S$48.4m, which

includes a deferred earn out consideration of up to S$18.3m. To simplify

things, I’ll just assume that a total of 48.4m was paid.

SATS also announced their intention to raise S$500m thorough

their MTN programme. To date, 300m has been raised, with 200m @ 2.88% p.a. and

100m @ 2.60% p.a., which I believe are reasonable borrowing rates and reflects

the financial stability of SATS. The remaining 200m of notes have not been sold

yet. Even if SATS were to raise up to 500m of debt, based on their total equity

of c.1.8b as at 31 Dec 2019, their debt to equity ratio would rise to 30-40%,

which is still reasonable to me. Hence, I believe that SATS can still tap the

debt markets if necessary. Personally, I would be comfortable with a debt to

equity ratio of up to 50-60%.

Therefore, if we were to estimate SATS’ cash level as of 31

March 2020, the ballpark figure would be 212m – 48.4m + 300m, which gives us a

total of $463.6m. Of course, this is assuming that the quarter from Jan to Mar

had delivered at least a net cash inflow, which is likely possible, because the

effects of the travel bans only started in March. Hence, if SATS’ burns cash at

a rate of 60-70m per quarter, they should still be able to last for at least

more than a year. If 200m more is raised, their cash runway then increases to

beyond 2 years.

3. Government wage subsidies and relief for rental & license fees

SATS currently benefits from some of the measures undertaken

by the govt to alleviate the impact on the aviation sector:

- 75% wage subsidy for local workers, capped at a

maximum salary of $4,600

- Subsidies for retraining of workers for redeployment

- License fees relief for ground handlers

- Rental relief for ground handlers

Given that the average salary of SATS’ employees was $52,304

in 2019, it would be reasonable to assume that a sizable proportion of their

workforce would be included in the JSS. The key assumption underpinning my

analysis of SATS would be the continued subsidies from the govt. This is

because SATS’ operating costs in an ordinary year is c.800m, hence without the

various subsidies, it is likely that SATS’ losses would be far greater than the

50-70m they projected for Q1 FY2021.

In their profit guidance dated 30th April, SATS’ projection

of a 50 to 70m loss for the quarter included the effects of govt subsidies,

hence a major assumption of my valuation would depend on the continuation of

these subsidies.

4. Food solutions and cargo flights are still operating

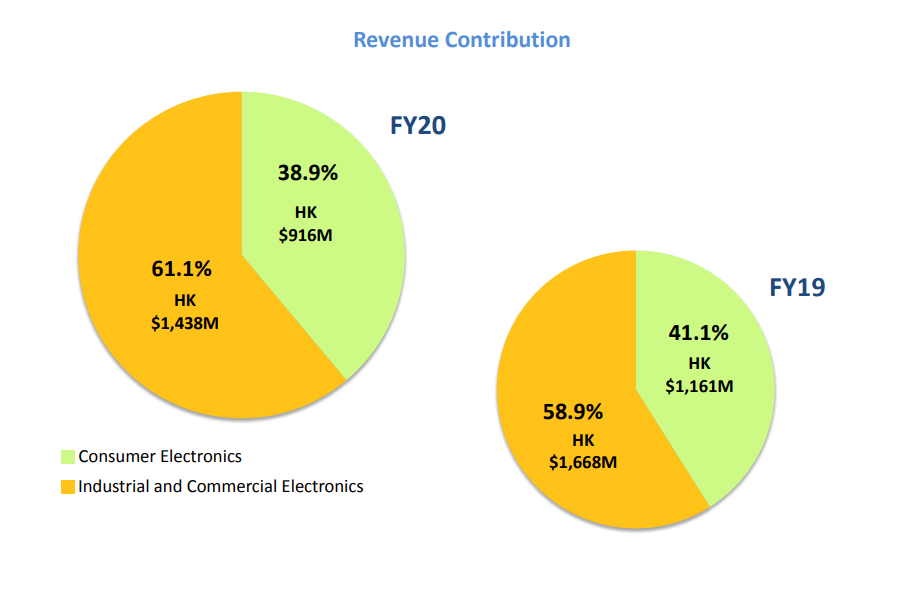

While c.65% of SATS’ revenue is derived from Singapore,

mostly from Changi Airport, (some from Marina Bay Cruise Centre), the few

bright spots for SATS would be that their food solutions segment and the

handling of cargo flights are still in operation. Air freight volume has fallen

by a lesser degree as compared to passenger volume, because cargo flights are

still necessary for the import and export of goods.

|

| Source: Changi Airport Traffic Statistics |

Recently, there was also news that SATS has started catering

meals for some of the quarantined foreign workers. This is positive for the

company, although the returns from this would probably be rather insignificant,

given that margins for food solutions tend to be lower.

5. Aviation remains a strategically important sector to

Singapore

During PM Lee’s latest speech, he mentioned that aviation

remains a strategically important sector to Singapore. “Air transport is

fundamental to Singapore's role as a global and regional hub.” SIA is

strategically important as our national flag carrier, and the govt has

indicated their intention to ensure that SIA survives this crisis. SATS plays a

crucial role in our aviation ecosystem too. Think about them as being similar

to Boeing for the US or Airbus for Europe – strategically important companies

that should be backed by the state during a crisis.

With Temasek being a major shareholder in SATS (39%), if

things get really dire, would we see them take corporate action, similar to

that for SIA? I don’t know, and I don’t wish to speculate.

Valuation

I used a simple DCF model to estimate SATS’ valuation. The

assumptions are rather straightforward, and I didn’t want to dive too deep into

the P&L projections because these are just ballpark figures.

The main assumptions are:

1. Covid lasts for 2 whole years – from FY2021 to FY2022

As SATS’ financial year starts from 1 Apr, that means 2 full

years of losses (cash burn) from 1 Apr 2020 to 31 Mar 2022. Think of that – no

overseas holidays until April 2022!

Beyond Apr 2022, hopefully, a vaccine is developed or we

achieve herd immunity. Air travel returns to pre-covid levels for FY2023.

2. Cash burn of S$250m for FY21 and S$250m for FY22

I derived the cash burn based on SATS’ projected 70m loss

per quarter – that implies a full year loss of 280m. However, this 280m loss

would reflect the accounting losses, hence we have to add back depreciation,

which is a non cash expense. For FY19, depreciation amounted to c.80m, which we

will add back. Additionally, capital expenditures are assumed to be 50m for

FY21 and FY22, on the assumption that capex would be scaled back due to the

crisis. Hence, that gives us a cash burn of 250m per year.

Again, I want to reiterate that these assumptions are based on

the expectation that SATS continues to receive govt subsidies.

3. Return to pre-Covid levels in FY23 (from April 2022

onwards)

Pre-Covid FCF was c.200m per year based on SATS’ annual

report. The discrepancy between the FCF, OCF and Capex is mainly due to SATS only

including ‘cash capex’ in their FCF calculations. Capex of 100m per year is

assumed.

|

SATS Cash Flows from FY15 to FY19

Source: SATS FY19 Annual Report |

4. Discount rate of 7.5% and terminal growth rate of 1.5%

To explain why I have chosen these inputs, the finance-y

answer would be: Due to SATS’ historically low beta, their more efficient

capital structure as a result of raising more debt, and in light of the lower

interest rate environment going forward, a WACC of 7.5% is derived.

But the short answer would be: Just use any discount rate

you’re comfortable with. For a comparison, DBS used a WACC of 5.7% and TGR of

3% in their SATS research dated 5 May 2020.

Conclusion

I have averaged down on SATS at $2.84, and it has become my

second largest position, at an average cost of $3.41. I believe that the long

term bet on aviation remains intact.

Additionally, it was reported that Changi

Airport would start to allow transit passengers from June 2, after the circuit

breaker ends, subject to strict measures. Hopefully, this would be the first

small step towards resuming airport operations. I await SATS’ results by 31

July 2020 for greater clarity.

Additional details not covered in my analysis:

1. Upside potential: Projection of revenue growth was

based on the assumption that passenger capacity at Changi Airport remains at

85m across 4 Terminals; the impact of T5 is not included, as I don’t believe that

it can be meaningfully estimated. Hence, the DCF derived value for SATS may

potentially be higher, if the increase in passenger capacity upon the

completion of T5 is included.

2. Downside risk: Bankruptcy of airlines resulting in

default of payments. SATS had $373.9m of receivables as at 31 Dec 2019. If certain

airlines go bankrupt, SATS may have to write off some of the receivables owed

by these airlines. Additionally, the solvency of SATS’ individual associates

were not considered. If some of their foreign associates/ subsidiaries do not

receive adequate government aid, they may be at risk of bankruptcies too.

If you are keen to learn more about SATS, do check out my other articles on the company:

Disclaimer: This article is intended for informational and discussion purposes only, and do not constitute financial advice. When in doubt, please contact a licensed financial adviser.

If you enjoy my articles, please 'Like' my Facebook Page at:

Follow me on Instagram at @AlpacaInvestments