The last time I wrote about Valuetronics was in late 2019,

when I published this article (Valuetronics Research). I had done some research on the company

as part of my internship application to an asset management firm. Subsequently,

Valuetronics’ share price climbed to a high of $0.86, before falling to a low

of $0.435 during the selloff in March.

After a strong recovery, Valuetronics’ share price tumbled

again this week, as the management guided for a poor outlook in the near

future, due to the renewed US-China trade tensions, which causes Valuetronics’

exports to the US to be subjected to tariffs ranging from 7.5% to 25%.

Consequently, management indicated that some customers in the auto and consumer

electronics segment were considering a switch of suppliers, and warned of

“significantly lower financial results in FY2021”.

Company Overview

| |

|

Valuetronics is an electronics manufacturer headquartered in

Hong Kong. The company provides integrated manufacturing, design, and

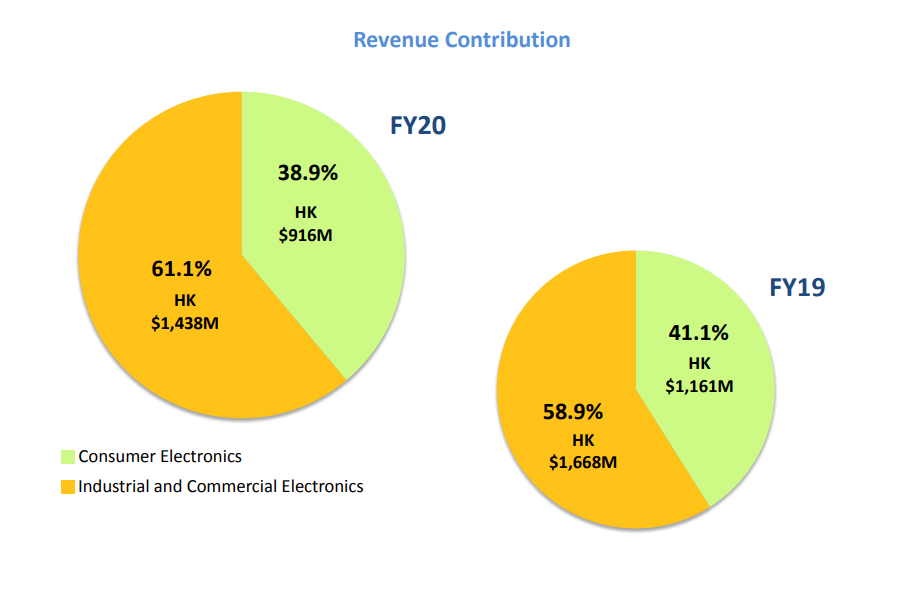

development services. It operates in two segments, the Consumer Electronics segment,

and the Industrial & Commercial Electronics segment. The CE segment

accounts for 39% of revenue, and 61% of revenue is derived from the ICE

segment. The company’s products include smart lighting, printers, automotive and

communications products.

FY2020 Earnings Review

Trade tensions have adversely impacted Valuetronics’ FY2020

results, as revenue declined by 16.8% from 2.83 bil HKD to 2.35 bil HKD, while

gross profit margin expanded slightly from 15.2% to 15.4%. Net profit fell from

199.5 mil to 178.9 mil HKD, a decline of 10.3%, while net profit margin

increased from 7.1% to 7.6%.

The positives

| |

|

Continued diversification out of China, with further

expansion in Vietnam ongoing. US-China trade tensions had an adverse impact on

Valuetronics, given that c.41% of the company’s revenue is derived from US

shipments.

Valuetronics has been working to mitigate the adverse impact

of tariffs by building up its production facilities in Vietnam. Mass production

at its Hanoi plant began in June 2019, while trial production at a second

facility started in May 2020. The company also acquired a plot of land in an

industrial park in Vietnam to build a manufacturing campus, which is projected

to commence mass production by 31 March 2022. This would further boost

production capacity, and diversification of its production base beyond China.

Robust balance sheet with a net cash position, reducing downside

risks. Valuetronics’ net cash per share stands at 44 cents, with a NAV of 50

cents. This compares with the closing price of 59.5 cents on Friday. With its net

cash position making up c.66% of its market capitalisation, downside risks

would be mitigated. However, it would be good to note that 200 mil HKD is

earmarked for the capex for their new facility in Vietnam.

The negatives

Escalation of US-China Trade War – Currently, c.41% of

Valuetronics’ revenue is derived from shipments to the US, which are subjected

to tariffs ranging from 7.5% to 25%. Further escalation in trade tensions may

pressure more customers to seek alternative suppliers.

Potential Upside?

Positive developments from the US-China trade negotiations –

Perhaps if Trump fails to get re-elected, this may be a positive for Valuetronics if trade tensions are resolved?

Valuation – Discounted Cash Flow

I didn’t want to go into the details of how the FCFF figures

were projected, because that would involve many detailed assumptions of revenue

drivers, expenses, margins etc. Thus, a high level view of estimating the future

FCFF would suffice instead.

The following assumptions were used for the Discounted Cash

Flow valuation of the company.

1. Drop in FCFF for FY21 and FY22 due to falling revenue as

more North American customers switch suppliers, followed by a recovery in FY23

due to the opening of the Vietnam campus in end FY22.

2. Discount rate of 10% to reflect the small cap premium as

well as uncertainty around longer term earnings. 0% terminal growth rate was

used as a conservative estimate.

3. FCFF of c.10 – 85m for the projected years, which is

significantly lower than the average of c.180m for the past 6 years. FCFF for

the past 6 years were fluctuating mainly due to the changes in working capital.

If we looked at cash flows before changes in working capital instead, we get a relatively

consistent number of 200 – 250 mil, with income tax paid of 10 to 20m annually.

4. Annual capex of 120m HKD for the terminal value, with

FY21 and FY22 at 150m to reflect the higher capex commitments of c.200m HKD for

the new Vietnam facility.

5. Cash of 800 mil HKD was used in the calculation of equity

value, to account for the 200 mil HKD earmarked for the capex in Vietnam.

With the above assumptions, a DCF derived price of $0.66 was

obtained.

Why P/E may not be meaningful

I think that while a P/E ratio is easy for investors to

understand, it may not be an appropriate metric to evaluate a contract

manufacturer like Valuetronics. Bear in mind that the following thoughts are

coming from a business student with zero knowledge of the manufacturing

industry, so please take them with a huge pinch of salt. For those with more in-depth

knowledge on the relationships between suppliers and customers in the

manufacturing industry, please let me know in the comments.

While I mentioned P/E as a valuation metric in my previous

article, I am currently of the view that P/E would not be a good valuation

metric, mainly because of the nature of the manufacturing industry. A P/E

valuation would be more reliable for companies with stable and predictable

earnings – for example, consumer stocks like Sheng Siong. However, while

Valuetronics’ earnings have been relatively stable over the past few years, the

certainty of earnings is questionable, because once a manufacturing

contract expires, the customer may switch over to another supplier if the costs

are lower. As we are witnessing currently, the certain customers have indicated

that they may switch suppliers due to the tariffs imposed on the shipments from

China. For Valuetronics, if earnings were to drop in a given year, using a P/E

multiple on that year’s earnings would give a significantly lower valuation.

Hence, to compare Valuetronics’ P/E ratio to a bunch of

peers like Venture Corp, AEM or UMS may not provide the best estimate of its

valuation, because of the each of these companies are vastly different.

Venture’s market cap is significantly larger than Valuetronics, thus Venture

may have greater bargaining power or economies of scale for production. For a

smaller manufacturing company, I believe that the firm would more likely be a

price taker, with less bargaining power when negotiating with larger customers.

Whereas AEM and UMS have extremely concentrated customers, which itself brings

about an entirely different set of benefits and risks.

Conclusion

|

| Source: Valuetronics FY20 Presentation |

I like the company as it has been operating very

conservatively by building up a huge cash buffer over the years. Before the

Covid-19 crisis, I have questioned the need for the company to build up such a

huge cash reserve, but I think the Covid-19 crisis has shown us the importance

of companies having a strong balance sheet. Valuetronics business has also been

incredible at generating positive free cash flows, which is what I look out for

in any business. As shown above, Valuetronics has managed to increase its

cash holdings from 689 mil to 1 bil HKD

over the past 5 years through its strong cash flows. This gives them the

ability to fund expansion plans without taking on any debt.

While earnings would be impacted in the short term, I

believe that any downside would be well supported by its net cash per share of

c.44 cents, while a successful diversification of its production facilities to Vietnam

would be beneficial to investors in the longer term.

Disclaimer: This article is intended for informational and discussion purposes only, and do not constitute financial advice. When in doubt, please contact a licensed financial adviser.

If you enjoy my articles, please 'Like' my Facebook Page at:

Follow me on Instagram at @AlpacaInvestments

Note: As of writing, I don't not hold a position on Valuetronics.

Disclaimer: This article is intended for informational and discussion purposes only, and do not constitute financial advice. When in doubt, please contact a licensed financial adviser.

If you enjoy my articles, please 'Like' my Facebook Page at:

Follow me on Instagram at @AlpacaInvestments

Hi, I just posted the same article a day earlier.

ReplyDeletehttps://www.rolfsuey.com/2020/06/finding-value-in-valuetronics-bn2si.html

Basically sharing similar views on the company.

One thing that you perhaps miss out is looking at the management team profile. For most time, we tend to focus on figures, but it is humans who drives the figures. Personally I think Valuetronics has strong management team. '

For PE, you have to compare across similar industry and similar company (competition in more direct manner). In the case of Valuetronics, there is little comparison available in SGX. You have to be in the industry with access to data of even private companies of Valuetronic's competitors to be able to compare.

Just my thoughts.