First off, wishing everyone a Happy Chinese New Year and a year of good health and wealth ahead.

“Hubris” (a

word I learnt watching “War Machine” on Netflix – a great movie by the way) is

probably the appropriate word to describe investors’ behavior leading up to this

months’ correction. Many were simply overconfident, and it wasn’t uncommon to

see people with 90%, 100% of their portfolios in crypto or hypergrowth stocks.

Some even claimed that annual returns of 50% or 100% should be the “new

normal”, and not the 7% to 10% historically. It all unraveled over the course

of the month, inflicting heavy damage on the very people who felt invincible in

the recent past. Evidently, everyone appears to be a genius during a bull

market, and it takes a sharp correction to differentiate luck from skill.

I myself am

not spared – my US positions took a heavy beating as well. But thankfully, my SG

positions cushioned the damage, while my HK positions were relatively flat. I

think the lesson here is diversification. If your portfolio is fully allocated

to a single asset class, a single region or a single factor, it is inevitable

that you’d experience a disproportionally large drawdown as compared to a

diversified portfolio. Over the long run, a concentrated portfolio may make you

higher returns if those bets turn out right. But you’ll have to stomach higher

volatility in the short run, and not everyone is prepared for that.

An

interesting observation I made over the past year was that when stock prices

see a quick and sustained rise, investors tend infer that the company is “good”

and “performing well”; conversely, when stock prices of the very same companies

decline, investors view the company as “bad” and “finished”. Yet, throughout

this process of the stock rising and falling (take many US hyper growth stocks

from May ’21 to present as examples), the underlying fundamentals of some

companies continued to grow. The takeaway here is not to draw conclusions from

the short term movements of stock prices – in the short term, the reasons for

stocks rising and falling are more driven by fear and greed rather than the

underlying financial performance; whereas in the long term, to would be more

reasonable to expect that stock prices are correlated with the fundamental

performance of the company.

Regardless

of the general somber mood, my overall portfolio has still held relatively

steady, down by a low single digit percentage. The recent selloff provides me

with the opportunity to accumulate mainly US Stocks/ETFs and SG Reits, which

have both been battered by the prospect of more rate hikes than expected.

My strategy

is to continue being selective in US Growth, while I am less bothered about my

ETF positions and simply continue to dollar cost average. The long term goal is

to build up a core portfolio consisting of mainly ETFs, then selecting single

stocks to generate alpha. As I’ve mentioned in my previous post, being a humble

fresh graduate means that for now, the effect of the monthly inflows from my

salary outweighs my investment returns.

For US

Growth companies, I mainly screen for fast growing companies that 1) have

little to no debt, 2) are profitable or at least cash flow positive, 3) trade

at valuations that are reasonable when compared to their historical valuations.

I am also taking advantage of the selloff in SG Reits to accumulate positions

for my dividend portfolio. For cryptocurrencies, I am still new to the space

and am keeping my allocation to this asset class small for now. But I think

tokens with actual use cases have great potential and am keen to learn more.

A quick

summary of the transactions for this month:

SG Reits:

Bought MCT and Lion Phillip S-Reit ETF

US Growth:

Bought UPST, PINS, TDOC

US ETF:

Started DCA on QUAL

Intl ETF:

Started DCA on IQLT

Crypto:

Bought SOL

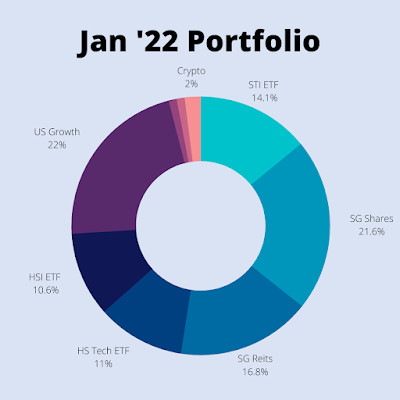

With these

additions, the current portfolio allocation looks like this:

SG Reits:

MCT, CLR

SG Stocks:

DBS, SGX, Valuetronics

US Growth:

BABA, PYPL, TTD, UPST, PINS, TDOC

Crypto:

BTC, FTM, SOL

US ETFs: QUAL

and IQLT are 1% each but I can’t seem to label them on the chart

Still

rather overweight on Singapore positions, but at the same time this is the very

reason why the portfolio has held up well YTD. Will continue to steadily add to

US Growth as I see many opportunities among beaten down stocks, while the DCA

process into ETFs is almost second nature to me at this point.

I’ve also

recently watched Jeremy Grantham’s interview with Bloomberg; I felt it was a

brilliant interview and I generally agree with many of the points that he

articulated. The full interview is 37 minutes long, but I would encourage you

to watch it. The two main takeaways from the interview were 1) When markets

peaked and crashed, there were prolonged periods of negative returns – Great

Depression (peaked in 1929, only recovered in 1954), Japan Asset bubble (1989

and yet to recover) and Dot Com bubble (peaked in 2000, only recovered in

2013), 2) US Equities are overvalued relative to the rest of the world.

Personally,

I think (1) can be somewhat mitigated by dollar cost averaging, which is what

I’ve been doing. For (2), it is really down to diversification and what one is

comfortable with.

To end off,

the US market had its worst start to a year since 2008, but I think there are opportunities

for long term investors to slowly start scaling up our positions. As long as

one has emergency funds set aside, practice diversification, and has a proper

framework for investing, I don’t think there’s much to fear even in this

current climate. As usual, invest prudently, and invest consistently. I’m

staying the course.

Going forward, I doubt I'd have the time to write lengthy blog posts, instead, I simply update my monthly portfolio on my Instagram page @alpacainvestments, so please follow me there if you want to keep up to date with my portfolio allocations.

No comments:

Post a Comment